FINANCIAL PLANNING We believe that before any advice is given, it is essential to understand all that is important to you and customize strategies around your objectives. We believe financial planning is a process and not a product. When determining the right approach for our clients, we find it paramount to understand the entire picture (investments, taxes, estate, etc).

Developing Your Road Map: Once you are confident in your goals, we will construct and maintain your personalized financial plan. This financial plan will serve as a road map going forward. Our comprehensive planning process seeks to provide you with the information you need in order to make prudent and well-informed decisions.

Cash Flow Analysis: Utilizing a statistical probability report called a Monte Carlo Simulation, we can help answer the question, “Will I have enough?” . Utilizing this analysis can empower you to make decisions by analyzing the impact certain financial choices may have on your financial future in various market environments.

Risk Assessment: After we analyze your financial projections, we then discuss any obstacles that could impact successfully achieving your goals and objectives. We review insurance, health care, investment risks, business risks, potential legal issues or other risk exposures that could compromise a positive financial outcome.

Monitor: Change happens and therefore monitoring is a critical part of every financial plan. We can periodically update your plan as tax laws, resources, goals and life events change. Planning is not a static process, but constantly evolving. We assist by helping you make confident financial decisions.

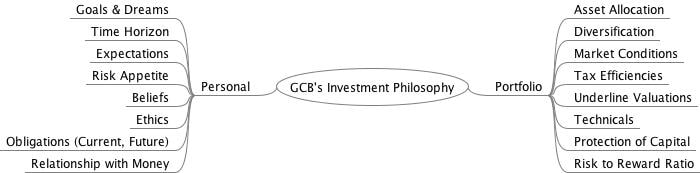

WEALTH MANAGEMENT Using our proven "Allocation Pie Process", GCB's investment approach is based on common-sense principles that integrate comprehensive financial planning with asset management. We focus on both the person as well as the portfolio. We first determine an asset allocation plan based on your overall goals, and tailor a portfolio specific to your needs. Thereafter, we implement with tax- and cost-efficient securities, integrate with other aspects of your financial situation, and dynamically adjust as circumstances warrant.

TAX PLANNING Wise tax planning is a crucial tool in protecting your hard-earned assets and allowing them to grow. We work closely with your accountants and other tax professionals. Together we can recognize important tax issues and provide you with a long-range plan that includes both the financial and tax perspective. We can help evaluate issues such as

converting all or part or your retirement plan to a ROTH IRA

maximizing your annual gift exclusion

contributing to a qualified retirement plan such as a 401(k) or IRA account

paying interest on certain debt such as student loans to reduce your adjusted gross income

Increasing tax deductions through charitable gifting

tax efficient investing

LIFE INSURANCE Insurance can be an important component to any retirement plan or strategy – but only if the situation warrants such use. Thus, we will evaluate your current insurance policies, as well as offer access to a broad array of life and long-term care insurance products and companies (we are not affiliated with any specific carrier).

401K PLANNING - Pension Consulting We specialize in building Employee Benefits Plans that meet YOUR needs. Nothing about you or your business is typical, and your benefits package shouldn’t be either. You need an intelligent, effective plan, custom-built to deliver value to your company, to your staff and their families – because you care and want to support those who are helping you build your vision for a better future.

GCB Private Wealth is a part of the employee benefits evolution, providing expert solutions through a team of advisors who operate with your best interests at heart.

ESTATE PLANNING You've spent a great deal of time and energy accumulating your wealth. A good estate plan keeps you in control of everything you've worked for and protects your interests and those of your loved ones. Flexibility, protection and the opportunity to preserve and increase wealth over multiple generations is the cornerstone of the estate plan.

In addition, we work closely with each client’s estate planning team to assist in developing an effective estate plan. Our estate planning practice can include the following personal and charitable trust services:

Personal & Charitable Trusts Revocable Living Trusts. A revocable or living trust is a trust that you can change or cancel during your lifetime. You control a revocable trust and the trust's earnings are consolidated into your income tax returns. You may continue to manage the assets, or your financial advisor will handle management of your assets under your supervision, and upon your disability. A revocable trust can also be used to transfer assets at death, similar to a will, yet without the formal, court-supervised process of probate, where it opens your estate to public scrutiny. Once you pass away, your wishes are final, and thus the trust becomes irrevocable.

Charitable Remainder Trusts.A charitable remainder trust is an irrevocable trust with both income and remainder interests. Income is paid to designated beneficiaries for a term or lifetime. The remainder interest is paid to qualified organizations as specified in the trust document when the trust terminates.

Charitable Lead Trusts.In a charitable lead trust, the trust pays a fixed percentage of assets to a qualified charity for either a set number of years or for the life or lives of the individuals. When the amount of the trust has ended, the remaining assets are distributed to the donor or heirs as noted in the terms of the trust.

Special Needs Trusts.Special needs trusts are often established by the parents or relatives of a disabled child, with funds to be used to pay for supplemental or living expenses of the disabled person not paid by other sources. Special needs trusts can also be set up with the disabled person's own funds, again to provide for supplemental medical or living expenses.

Irrevocable Trusts.An irrevocable trust is a trust that cannot be changed or cancelled at any time. This trust is a separate legal entity and its own taxpayer. The terms of many irrevocable trusts, however, allow tremendous flexibility. While many irrevocable trusts come into being at death, irrevocable trusts set up before death are often used to hold life insurance policies, gifts of assets to be available to beneficiaries at a future time, or funds for future charitable contributions. To achieve beneficial tax results, many irrevocable trusts are written to follow patterns based on the rules in the Internal Revenue Code. The structure most suited to your needs can best be determined with the help of financial, legal and tax advisors who specialize in this field.

Agency Relationships.Agency relationships can be set up for any of the above account where the fiduciary or fiduciaries designate an agent to undertake one or more of the responsibilities for the account.

Private Foundations.A private foundation is a charitable organization created and funded by a donor as a trust or a non-profit organization, which is designed to achieve one or more specific charitable functions.

Guardianships. Guardianships are established to protect and handle the assets of minors.

Rabbi Trusts. Rabbi trusts are set up by corporations to support non-qualified, deferred compensation plans.

Irrevocable Life Insurance Trusts. An irrevocable life insurance trust (ILIT) is typically used to shelter an insurance death benefit from estate taxes and may provide liquidity to pay estate taxes and settlement costs. A trust is created, and then the trust purchases and owns a life insurance policy. Upon death, the insurance proceeds are paid out in accordance with the terms of the trust.